4 Home Remodeling Projects with the Highest ROI

Ask any homeowner about what they would like to change about their home, and most will say, “How much time do you have?

Home improvements (cue Tim Allen) or home remodeling projects can stem from a variety of motivations, like preparing your home to put on the market, adding space for a growing family, addressing outdated features or aesthetics, or fixing structural/functional issues with the home.

However, when it comes to home remodeling projects, too many people assume their project will proportionally increase the value of their home. Few actually consider the complete scope of return on investment (ROI), taking into account not only potential impact on resale value but also the total costs of time, labor, and materials. Some renovations may provide more “quality of life” ROI by improving comfort and aesthetics without significantly impacting resale value, while others can deliver notable financial returns.

Whether you’re looking to upgrade your living space, increase the equity of your home, or trying to make some quick changes to improve your resale price, here are four remodeling projects with the highest ROI and some tips on how to get them done.

Top 4 Home Remodeling Projects with the Highest ROI

Before diving into specific projects, it’s important to understand how the data supporting these ROI estimates was gathered. This article references findings from the 2024 Cost vs. Value Report conducted by Zonda Media, a reputable research firm in the real estate and construction industries. The report’s ROI figures are based on national averages for both the cost of materials and labor, which means that regional differences may lead to variations in actual returns.

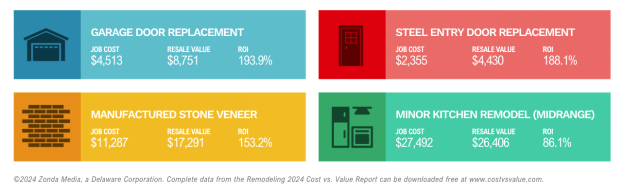

1. Garage Door Replacement

- Job Cost: $4,513

- Resale Value: $8,751

- ROI: 193.9%

Replacing an old garage door is one of the simplest ways to dramatically boost your home’s curb appeal—and it happens to deliver the highest ROI of any remodeling project. The impact is largely due to the prominent visual space a garage door occupies on a home’s exterior. A sleek, modern garage door can make your entire facade look fresher and more attractive to buyers.

Garage doors with the highest ROI include insulated steel doors with modern paneling, custom carriage-style doors, and those featuring windows or decorative hardware. These options not only enhance the home’s exterior aesthetics but also improve functionality and energy efficiency.

2. Steel Entry Door Replacement

- Job Cost: $2,355

- Resale Value: $4,430

- ROI: 188.1%

Upgrading to a steel entry door is a simple yet impactful change that can drastically improve both the look and energy efficiency of your home. Steel doors cost less than wood ones, giving you a cost effective way to make a big impact on the curb appeal of a home, without sacrificing performance, life span, or durability.

Why It Works:

- Cost-Effective Curb Appeal: Steel doors are less expensive than wood but provide a similar aesthetic boost. This makes them a budget-friendly way to enhance a home’s exterior.

- Energy Efficiency: Many steel doors come with insulating cores, which can help keep your home comfortable year-round and lower energy bills.

- Increased Security: Steel doors are harder to break into, providing an added layer of safety that appeals to security-conscious buyers.

3. Manufactured Stone Veneer

- Job Cost: $11,287

- Resale Value: $17,291

- ROI: 153.2%

Manufactured stone veneer (MSV) is a high-ROI project because it delivers a striking visual upgrade at a relatively moderate cost. MSV is an artificial cladding material designed to mimic the look of natural stone, making it a cost-effective way to add texture and sophistication to your home’s exterior.

Why It Works:

- Strong Visual Impact: Stone veneers add depth and elegance, creating an upscale appearance that can significantly boost curb appeal.

- Durability and Low Maintenance: Unlike natural stone, MSV is lightweight, easier to install, and resistant to wear and tear.

- Perceived Value: Even though it’s a faux material, MSV adds an air of luxury and craftsmanship that can make your home more appealing to buyers.

Pro Tip: Use manufactured stone veneer to accentuate specific areas, such as around the entryway or along the lower portion of the facade, for maximum visual impact without overspending.

4. Minor Kitchen Remodel (Midrange)

- Job Cost: $27,492

- Resale Value: $26,406

- ROI: 96.1%

According to Homelight’s “Top Agent Insights End of Year 2024 Report”, “88% of agents say that upgraded kitchens and appliances are one of the best selling points for homes”--a significant increase from the previous year. https://homelightblog.wpengine.com/wp-content/uploads/2024/12/homelight-top-agent-insights-end-of-year-2024-report.pdf

The trick to ROI with a kitchen remodel is the budget, and how you decide to balance what to upgrade, the quality of materials, and how much to work within the existing layout. For example, you can make a big impact with less expense if you keep your current cabinet boxes but upgrade the doors and hardware. However, if you strike that balance, you can recoup much of your investment. If you’re looking to sell, an updated kitchen will appeal to buyers, which can also help your home stand out and sell faster.

Why It Works:

- High Buyer Interest: Kitchens are a focal point for most buyers, so even modest improvements can make a significant impact.

- Affordable Upgrades: By focusing on midrange materials—such as quartz countertops, midrange appliances, and refaced cabinets—you can keep costs manageable while still delivering a fresh look.

- By keeping the existing layout and avoiding costly structural changes, you can modernize your kitchen while keeping costs down.

Key Takeaways for Homeowners

7 out of the 10 best ROI projects all have to do with improvements to the exterior of your home, which makes one thing very clear: Boosting the curb appeal of your home in a cost-effective manner will give you the best ROI if you’re thinking about selling this year.

If you look at the current housing market, you can start to see why that is. In the post-pandemic frenzy, buyers had to accept whatever they could find. However, housing inventory has increased over the last couple of years, giving buyers more options. Additionally, due to high-interest rates and affordability issues, the current market favors older, move-up home buyers who are sitting on equity, and these buyers can afford to be pickier about the home they buy.

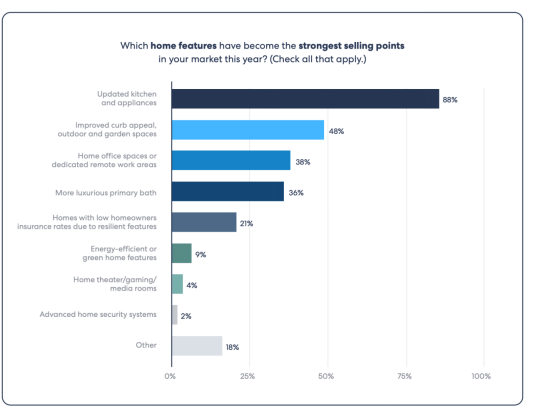

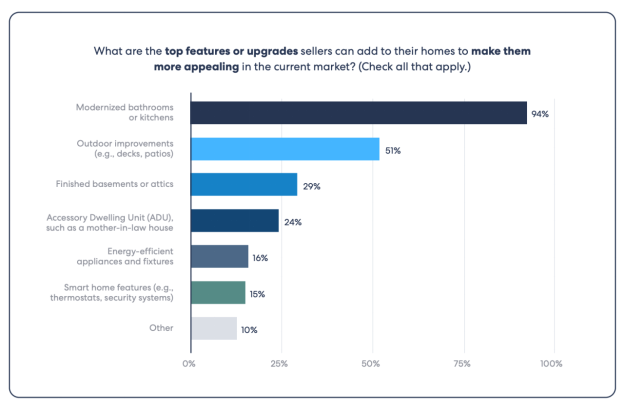

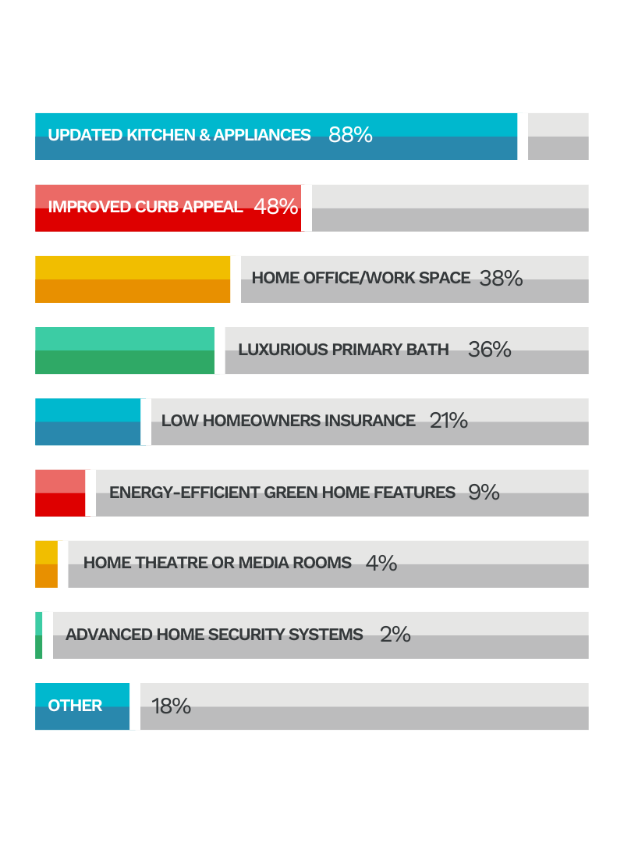

You can see these trends play out in the “Top Agent Insights End of Year 2024 Report” conducted by HomeLight:

Given these trends, it’s no wonder that the remodeling projects with the best ROI are those that make the home stand out from other homes in the area and leave a strong impression with potential buyers.

Conversely, the projects with the lowest ROI involve major remodels or upscale materials. Anytime you alter the footprint of a home—such as by moving walls or adding square footage—you’ll incur higher costs and lower returns. Unless you’re a general contractor or a skilled DIYer, these high-end renovations typically aren’t worth it from a purely financial perspective. The one caveat is if you’re in a market where high-end appliances and materials are the rule not the exception.

How to Get Started on a Remodeling Project

Starting a remodeling project can feel overwhelming. Here’s how to set yourself up for success:

1. Outline Your Project Goals

Before you dive into the nitty-gritty of remodeling, take a step back and clarify what you hope to achieve.

Are you remodeling to improve aesthetics? To improve functionality or comfort for your family? To prepare your home for the market or boost your resale value? Is it an essential repair? After you decide on why you’re doing it, you can take a step back and decide what is worth the cost to you.

2. Get inspired:

Take time to gather ideas and give shape to your vision. Whether you're updating a single room or tackling a whole-house remodel, these resources can inspire you:

- Houzz – A go-to platform for home remodeling ideas, complete with photos, product links, and even local contractor recommendations.

- Pinterest – Create mood boards for different rooms by pinning your favorite designs and layouts. You can also add '-pinterest' to Google searches to find more targeted boards and collections of remodeling ideas on Pinterest.

- This Old House – Packed with articles, videos, and guides on home renovation projects, from DIY fixes to large-scale remodels.

- YouTube Channels: Follow popular home renovation YouTubers who share real-life projects, product reviews, and practical tips.

- Visit Local Showrooms: You can visit the showrooms or warehouses from local manufactures for ideas on fixtures, cabinetry, and counter tops.

- Open Houses - Stop by open houses in your area to get a feel for what’s popular and what other homeowners have done.

- Local Remodeling / Contractor Websites: Many will post galleries and before/after images of their renovations, and these galleries can be a goldmine for practical remodeling ideas!

3. Prioritize your wants vs. needs: Once you’ve gathered ideas, it’s time to separate the essentials from the extras.

- Must-Haves: These are the non-negotiable items—structural fixes, code-compliance upgrades, or critical repairs.

- Nice-to-Haves: These are aesthetic choices or features that you’d like to include if your budget allows.A prioritized list will help you make tough decisions if costs start to climb or timelines get tight.

4. Create a scope and timeline: Clearly defining what’s included (and excluded) in your remodel is critical for staying on schedule and within budget.

- What’s Included: Are you only updating finishes and fixtures, or are you changing the layout and moving walls?

- Project Phases: If you’re remodeling multiple areas, consider breaking the project into phases to manage timelines more effectively.

- Expected Timelines: Be realistic about how long the project will take, especially if you’re working around major life events or seasonal weather.

5. Set a realistic budget: Start by researching the typical costs for your specific type of remodeling project in your area. Resources like Remodeling Magazine’s Cost vs. Value Report, HomeAdvisor, and NAHB provide national and regional averages for popular renovations like kitchens, bathrooms, and additions.

6. Include a Contingency Fund: Even with thorough planning, unexpected costs seem to always arise. Many experts recommend setting aside 15% - 30% of your total budget for contingencies.

7. Research contractors & Get Multiple Quotes: If you're hiring contractors, request at least three detailed quotes to compare prices and scope of work. Make sure to clarify what’s included in each quote to avoid misunderstandings. And use your checklist below for some tips on hiring a contractor!

Checklist for Hiring a Contractor

Finding the right contractor is crucial for a successful remodeling project. Here’s a quick checklist to help you hire the right professional:

- Get recommendations from friends, family, neighbors, and your real estate agent. Word of mouth is one of the most reliable ways to find a trusted contractor. Ask people you trust about their experiences and if they would hire the contractor again. After you have a recommendation, you can also search for reviews online.

- Check credentials, licensing, and insurance. Verify that the contractor is licensed to work in your state. Most states have an online database for checking contractor licenses. You can also look for contractors certified by reputable organizations, such as the National Association of the Remodeling Industry (NARI).

- Review past projects and ask for client references. Ask to see a portfolio of previous projects similar to yours. Pay attention to the quality of work and whether their style aligns with your vision.

- Request detailed bids from multiple contractors. Ask for written estimates that break down costs into categories such as labor, materials, permits, and any additional fees. Compare bids carefully to ensure all contractors are quoting on the same scope of work.

- Ensure the contract includes a clear scope of work, timeline, and payment terms.

- Check references - A reputable contractor should have no issue providing references. Contact past clients and ask about their experience.

- Avoid red flags

- Unusually Low Bids: If a bid is significantly lower than others, it could indicate corner-cutting or hidden costs.

- Pressure to Pay Upfront: A small deposit is normal, but never pay the full amount before work begins.

- Lack of Written Contract: Never agree to verbal agreements only.

- Poor Communication: If a contractor is difficult to reach or dismissive during the bidding process, this may continue during the project.

Conclusion

Whether you’re updating your home to sell or simply want to enjoy a more modern space, focusing on high-ROI projects is a smart strategy. From replacing your garage door to enhancing your home’s exterior with stone veneer, these upgrades can boost both your home’s value and appeal.

Curious about what features are popular in your neighborhood? Thinking of moving and wondering what remodeling projects, if any, you should do before listing? Want recommendations on contractors? I’m happy to help!