Home for the Holidays: How To Stretch Your Budget in a Season of Inflation

Home for the Holidays: How To Stretch Your Budget in a Season of Inflation

You don't have to break the bank to celebrate the holidays in style—even in this season of inflation. Prices may be higher on everything from food to gifts to decorations, but there are still plenty of opportunities to eke out extra savings.

For example, according to the U.S. Environmental Protection Agency (EPA), you can save a couple of hundred dollars a year just by sealing your home and boosting its insulation.1 Other small fixes—such as swapping old light bulbs for LEDs and plugging electronics into a powerstrip—can boost your yearly savings enough to pay off some of your holiday budget.

And thanks to a pandemic-era boom in online shopping, it is easier than ever to find deals on new and pre-owned furniture, thrifted gifts, DIY decor, and more. Even secondhand stalwarts like Goodwill have joined the digital fray, making it a cinch to score gently-used treasures at extra-low prices.2

You won't be the only one bargain-hunting your way to a more financially-stable New Year. Multiple surveys have found that inflation is not only chilling people's spending, it's also prompting shoppers to search for better deals and creative ways to reduce their bills.3

Here are some strategies you can use to boost your holiday budget by trimming household expenses:

- Hunt for Deals on Groceries

If you're finding it harder than it used to be to serve your family dinner on a budget, you're not alone. With the U.S. food-at-home index (a measure of grocery price inflation) at a 43-year high, many families are struggling to control costs on food staples, such as meat, dairy, produce, and grains.4

That's made pulling off holiday gatherings especially stressful lately. But don't despair: Even with inflation, retailers are still giving motivated shoppers plenty of opportunities to whittle down their bills.

The key is to pay attention to the cost of each item on your shopping list—not just the most expensive—and look for easy swaps and discounts. For example, try buying non-perishable items in bulk, especially when they’re on sale, and only in-season produce. Or trade name-brand goods for less expensive options from a store's private label. As you tap into your inner bargain hunter, you could be surprised by what you save when you’re more mindful of your selections.

And unlike in the old days, you no longer have to clip your way through paper flyers to snag a bargain. Instead, you can save both time and money by scouting for deals online, digitally clipping coupons, and earning cash back through special apps and browsers. For example, coupon aggregation sites, like Coupons.com, and shopping apps—such as Checkout 51 and Ibotta—make it easy to score discounts and cash back on a variety of purchases, including groceries.

Also, check to see if your neighborhood grocer posts their weekly flyers online. If you're hosting a holiday party, the markdowns you find can help you narrow your food and recipe choices, based on what's currently on sale.

2. Prep Your Home for Holiday Guests With Pre-Owned Finds

You don't have to sacrifice style for the sake of preserving your holiday budget either. If you're expecting company this year and would like to add some festive flair to your home, you can do so inexpensively—especially if you're willing to decorate with items that are secondhand.

Thrifting is back in vogue, with an increasing number of shoppers preferring pre-owned furniture and home goods. A recent study found that the “recommerce” market grew almost 15% last year, which was twice the pace of general retail.5 Plus, buying used isn’t just a great way to save money, it also helps the environment by keeping reusable items out of landfills.

Fortunately, it’s become easier to score secondhand deals online. For example, you can scout consumer marketplaces on Facebook, Craigslist, and OfferUp. Or you can take advantage of neighborhood freecycles and “Buy Nothing” groups. And a number of thrift shops now have e-commerce sites, including major chains, like Goodwill.

If you're handy with a paintbrush or have some basic carpentry skills, you can also modernize some of your existing furniture by upcycling it yourself. Or, if you enjoy crafting, search through your own recycling or sewing bin for raw material to make one-of-a-kind decorations.

Don't stress yourself out, though, if you don't have the time or money to dress your home the way you hoped. “A house doesn’t have to be perfect or completely done for it to feel festive or inviting,” designer Justina Blakeney noted in an interview with the Washington Post. “These are family and friends, and they are not judging you.”6

3. Forgo Major Renovations in Favor of DIY Home Improvements

Holidays are always a tricky time to undergo big renovations. But with ongoing worker and material shortages, now is an especially bad time to commit. Inflated costs can add thousands to your reno budget –—and unnecessary stress to your holiday.

Instead of suffering through an ill-timed remodel, you're better off saving this time of year for simpler, less expensive projects you can do yourself.

One winter-perfect upgrade to consider: Build a DIY fire pit so that you and your guests can roast marshmallows and relax in the cozy comfort of your backyard. You can also add some extra ambiance by hanging energy-efficient LED outdoor string lights that change from white to colorful. These are festive enough for the holidays, but also versatile enough to use year-round.

Or, if you'd rather curl up by an indoor fire, channel your DIY energy into a fireplace upgrade. Adding a wooden beam to the top of your mantel can add an extra layer of coziness. Alternatively, re-tiling or painting your fireplace surround can lend contemporary flair.

Just be sure to stick to DIY projects that you know you can do a quality job on—especially if your changes will be difficult to reverse. Feel free to reach out for a free assessment to find out how your planned renovations could impact your home’s resale value.

4. Invest in Home Maintenance Projects That Cut Your Utility Bills

You can save money by completing basic home maintenance tasks[1] , such as swapping your furnace filter and updating your lightbulbs. But if you really want to lower your bills this winter, consider projects that make your home more energy efficient.

According to the EPA, 9 out of 10 homes in the U.S. are under-insulated, which wastes energy and money.7 Luckily, there are plenty of DIY insulation projects that you can complete in just a few days. For example, the EPA offers guides on how to:

● Insulate your attic or basement crawl space

● Weatherstrip doors and windows

● Seal areas around the house that may be leaking air, including electrical outlets and fireplaces

The savings you get from these projects can really add up. The EPA estimates that sealing and insulating your ducts can make your HVAC system up to 20% more efficient.8 And thanks to new provisions from the Inflation Reduction Act, you can also save a bundle this year by investing in certain energy-efficient upgrades and claiming a tax credit.9 Be sure to check with us about any local rebates and incentives that may be available, too, before getting started on a project.

5. Use Expense Tracking to Boost Your Holiday Budget

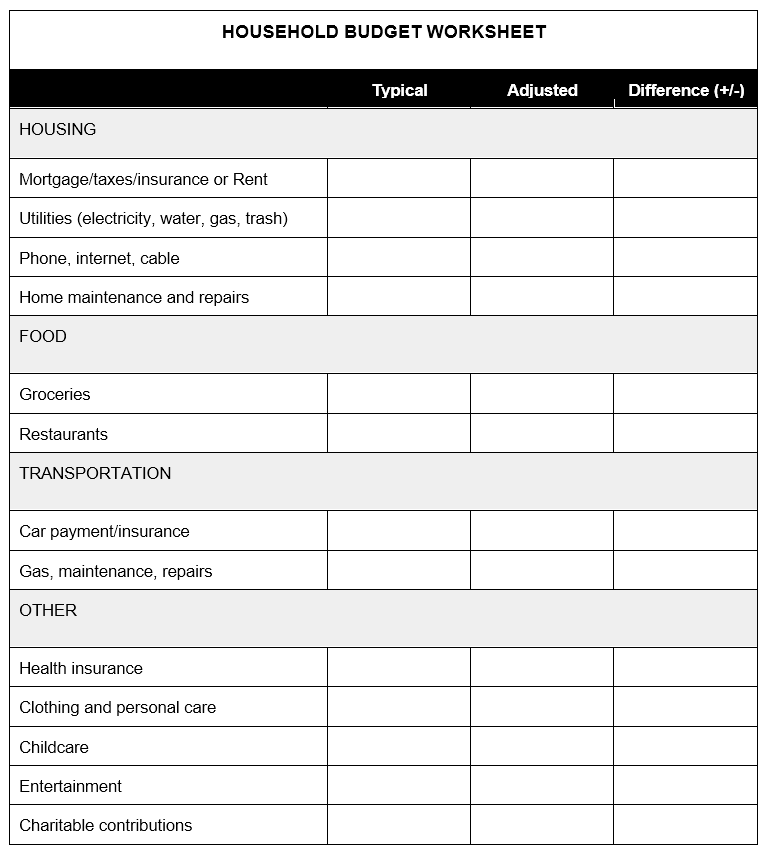

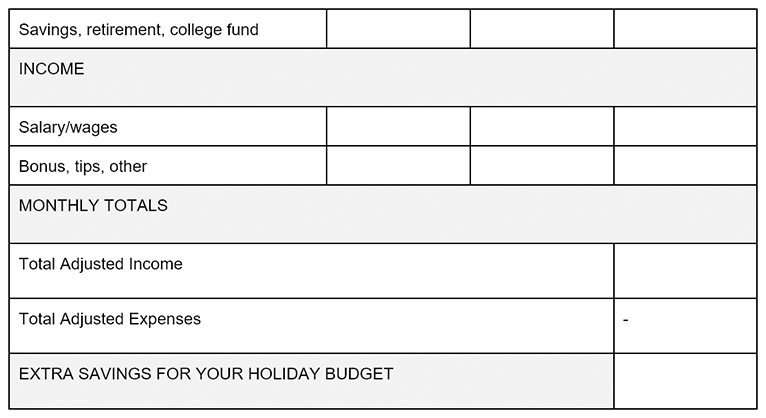

To avoid overextending yourself during the holidays, one of the best things you can do is track your income and expenses. If your monthly budget is usually tight, you may need to make some adjustments to free up cash for holiday expenditures.

For example, here's a sample budget worksheet that we created. Start by adding in your expenses: Under the “Typical” column, you can list your standard expenses, and under the “Adjusted” column, list any areas where you could cut back on spending.

Then consider how your standard wages may be adjusted this month by extra shifts, additional tips, or an end-of-year bonus. By decreasing your spending and/or increasing your income, you can build room in your budget for holiday gifts and gatherings.

Household Budget Worksheet

Feel free to utilize this worksheet as a template that you can personalize to your needs, or ask us for a PDF copy that you can print out and use right away.

WE’RE HERE TO HELP

We would love to help you meet your financial goals now and in the year ahead. Whether you want to find lower-cost alternatives for home renovations, maintenance, or services, we are happy to provide our insights and referrals.

And if you’re saving up to buy a new home, we can help with that, too. This is the perfect time to score a great deal because only the most motivated homebuyers and sellers are active in the market right now. So reach out to schedule a free consultation. We can fill you in on some of the exciting programs and incentives we’re seeing that help make homeownership more affordable.

The above references an opinion and is for informational purposes only. It is not intended to be financial, legal, or tax advice. Consult the appropriate professionals for advice regarding your individual needs.

Sources:

1. U.S. Environmental Protection Agency (EPA) - https://www.energystar.gov/campaign/waysToSave#!card0-GW91

2. USA Today - https://www.usatoday.com/story/money/retail/2022/10/05/goodwill-launches-online-store-goodwillfinds-website/8185084001/

3. Retail Dive -

https://www.retaildive.com/news/inflation-drives-shopping-changes-consumers-survey/629973/

4. NBC News -

https://www.nbcnews.com/select/shopping/how-save-groceries-ncna1299053

5. CNBC - https://www.cnbc.com/2022/09/14/secondhand-shopping-is-booming-heres-how-much-you-can-save.html

6. Washington Post -

https://www.washingtonpost.com/home/2021/11/09/holiday-entertaining-tips/

7. U.S. Environmental Protection Agency - https://www.energystar.gov/campaign/seal_insulate/why_seal_and_insulate

8. Energy Star -

https://www.energystar.gov/campaign/waysToSave

9. The White House -

https://www.whitehouse.gov/cleanenergy/?utm_source=cleanenergy.gov

Extra blog graphic quote: Save money by completing home maintenance tasks and projects