Real Estate Market Update: What Mid-Year Indicators Mean for Your Next Move

As we reach the midpoint of 2025, the U.S. housing market stands at a critical juncture. The frenzy of the pandemic-era real estate boom has long since cooled, but in its place we’re seeing a market searching for balance. Higher mortgage rates, cautious buyers, and rising home inventory are combining to reshape what it means to buy or sell a home in today’s climate.

“The housing market is at a turning point,” says Nadia Evangelou, senior economist and director of real estate research at the National Association of Realtors.1 This turning point brings both challenges and opportunities. Whether you’re buying, selling, or just keeping a close eye on the market, understanding these evolving trends is essential.

In this comprehensive market update, we examine four key factors influencing today's housing market and provide actionable strategies for navigating these evolving conditions.

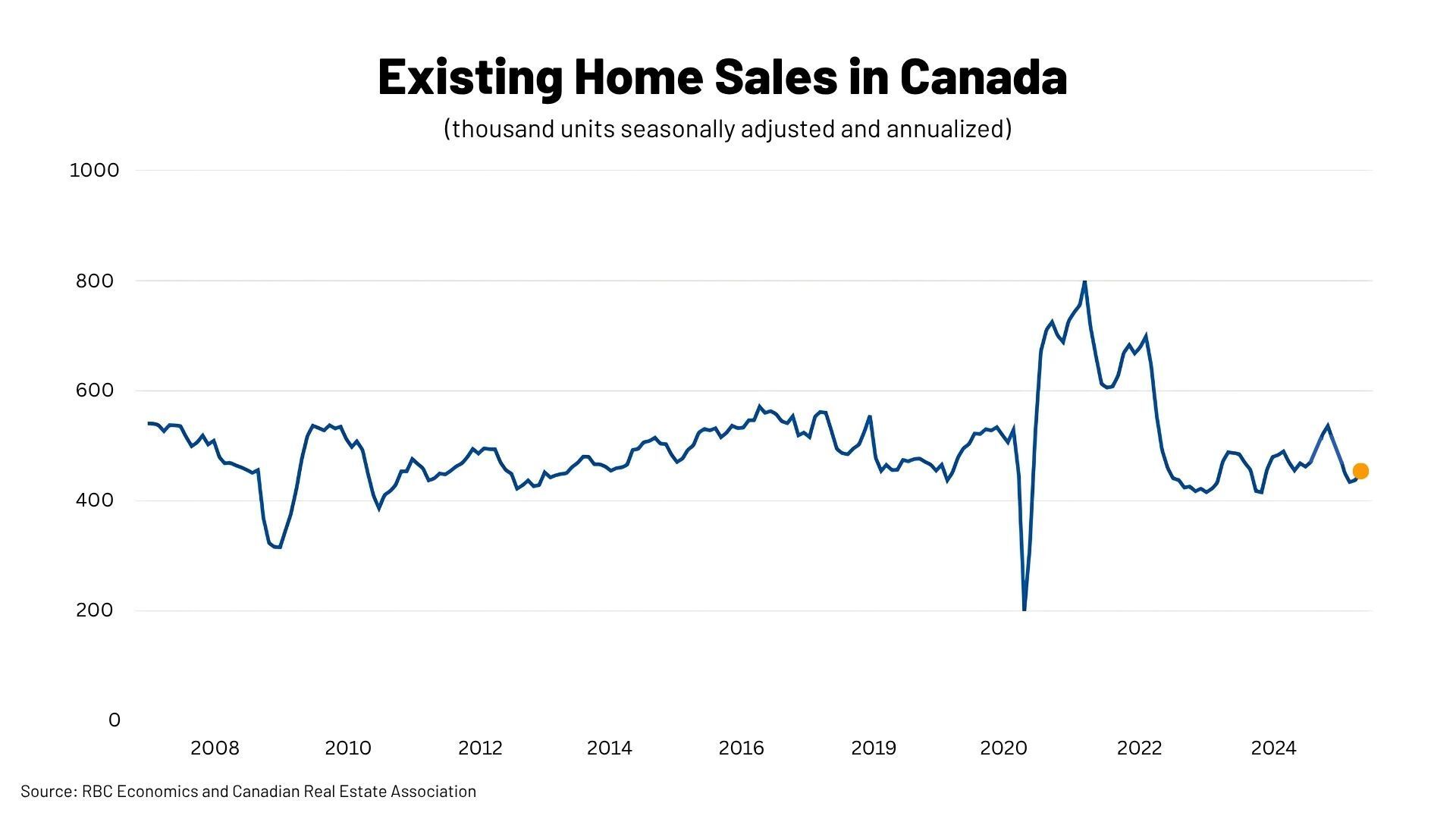

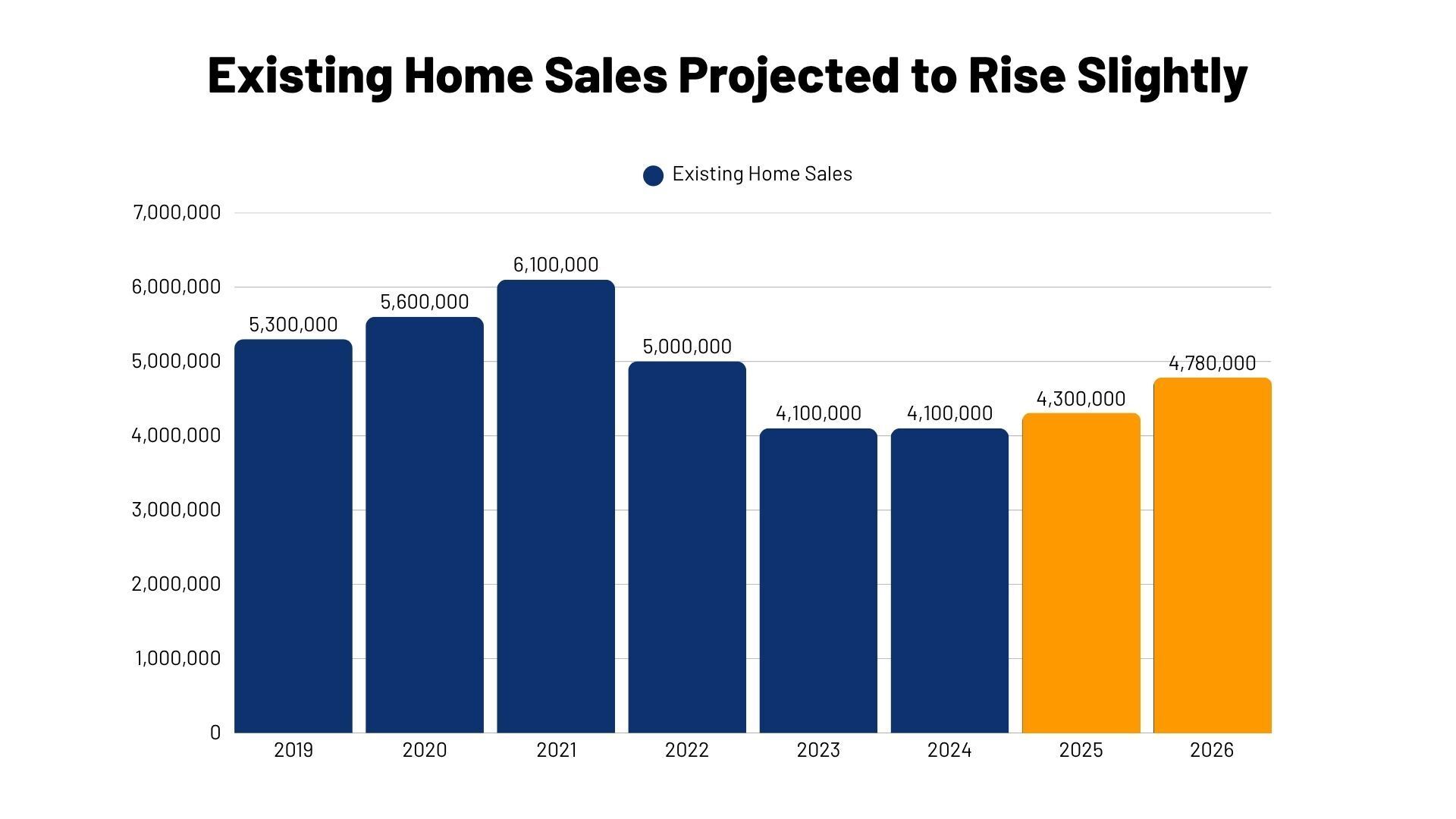

FEWER HOME SALES, BUT MOMENTUM IS GROWING

While existing home sales have seen a modest uptick compared to last year, overall activity remains well below pre-pandemic norms.2,3 Many potential buyers are still on the sidelines, held back by ongoing economic uncertainty and affordability challenges driven by elevated mortgage rates and home prices.4

As Lawrence Yun, Chief Economist for the National Association of Realtors, explains, “Home sales have been at 75% of normal or pre-pandemic activity for the past three years, even with seven million jobs added to the economy. Pent-up housing demand continues to grow, though not realized. Any meaningful decline in mortgage rates will help release this demand.”3

Yet, change is in the air. An increase in inventory, coupled with selective price reductions, is creating renewed interest among buyers. Hannah Jones, senior economic analyst at Realtor.com, told Newsweek in May, “This summer’s housing market is expected to display familiar seasonal patterns, such as increased home sales and rising prices, but overall activity may remain subdued as buyers contend with elevated housing costs.”5

What it means for you: A slower pace of sales offers opportunities for buyers. With less competition and more room to negotiate, now could be a smart time to reenter the market.

For sellers, success lies in understanding today’s buyer mindset and pricing your home to reflect current market dynamics. We're here to help you analyze local trends and craft a strategy that gets results.

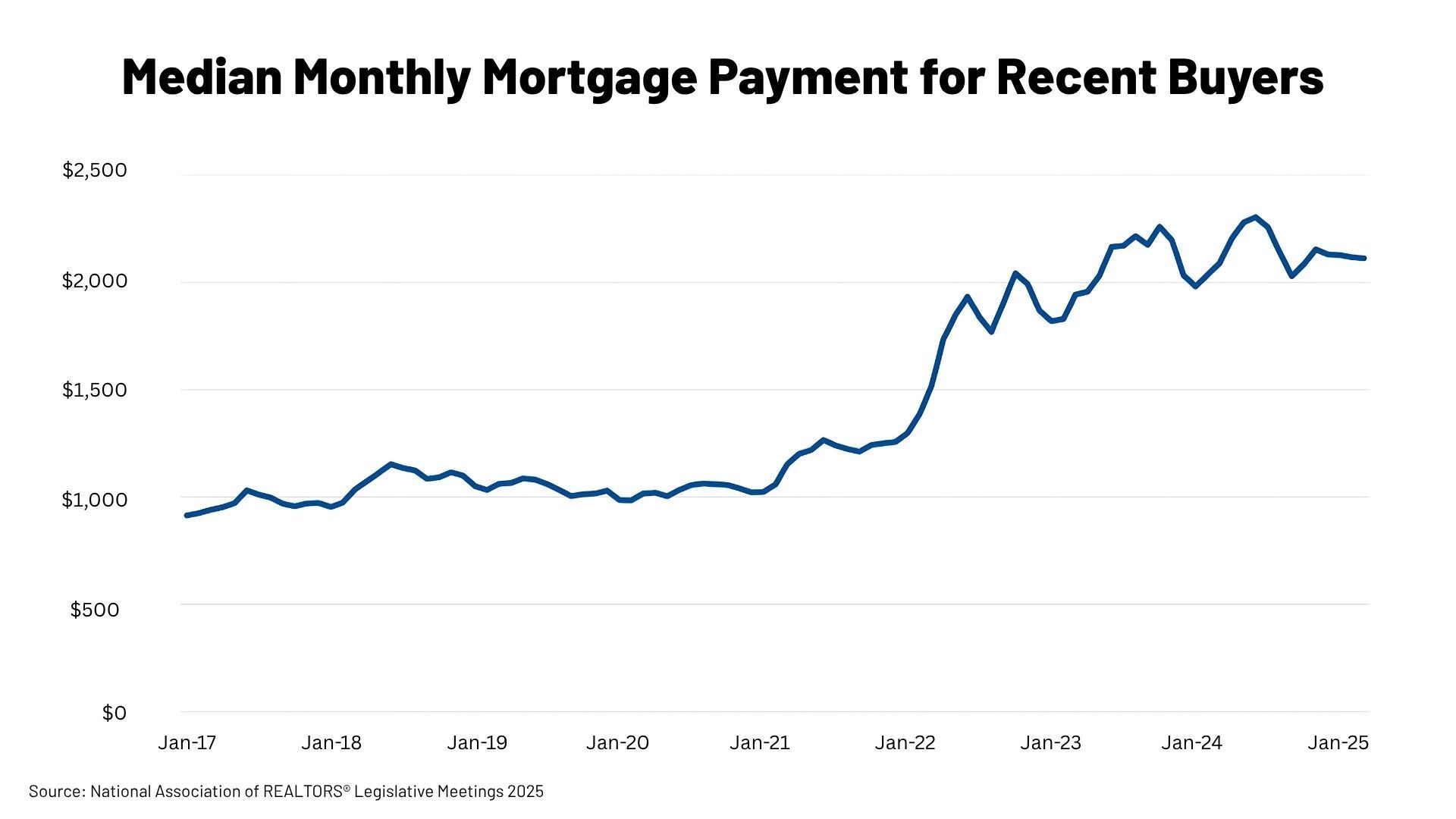

MORTGAGE RATES REMAIN ELEVATED BUT STABLE

Currently, 30-year fixed mortgage rates are hovering below 7%, and Yun expects them to average 6.4% in the second half of the year.6 While this is a far cry from the sub-3% rates of the pandemic era, it’s becoming the new normal. “Persistently high mortgage rates mean affordability remains top of mind,” explains Jones.5

For many would-be buyers, affordability challenges are now central. Monthly housing payments have more than doubled since the pandemic, not only due to higher home prices but also because mortgage rates are amplifying the cost of borrowing.7 In response, builders and sellers alike are offering concessions—from interest rate buydowns to closing cost assistance.8

What it means for you: Mortgage rates aren’t likely to drop significantly anytime soon, so waiting for a better rate might not be the most effective strategy. Instead, buyers should focus on ways to reduce costs upfront or refinance later if rates eventually fall.

Sellers take note: Offering mortgage rate incentives or closing cost support can set your listing apart and expand your pool of qualified purchasers. We can help you evaluate your options and market these perks to today’s cost-conscious buyers.

AN UPTICK IN INVENTORY OFFERS OPPORTUNITY FOR BUYERS

One of the most significant shifts in 2025 is the dramatic change in housing supply. For the first time in recent history, there are far more active sellers than buyers—an estimated 33.7% more.

This reversal stems from a combination of factors: the return-to-office trend has cooled demand in previously hot markets, while affordability issues continue to keep many potential buyers on the sidelines. At the same time, a growing number of homeowners—tired of waiting out market uncertainty—are choosing to list their properties, further swelling the supply.9

Many major metros are now considered buyer’s markets, especially in the South and on the West Coast. Homes are sitting on the market longer, and stale inventory is piling up. “The balance of power in the U.S. housing market has shifted toward buyers,” says Redfin senior economist Asad Khan.9

What it means for you: Buyers in many markets now have more choice and leverage than they’ve had in years. Sellers must adapt quickly—pricing aggressively, staging well, and being open to negotiation.

A skilled agent is an invaluable ally in this climate: For buyers, we can help identify hidden gems and guide strong offers. For sellers, we can develop marketing strategies to move your home efficiently, even in a competitive landscape.

HOME PRICES REMAIN HIGH BUT SHOW SIGNS OF SOFTENING

After years of rapid price growth, the market is seeing a gentle descent back to earth. While some pockets of the Northeast and Midwest are still experiencing price increases, values are flattening or falling in many parts of the country. Newsweek reports that home values declined in over half the U.S. states during the first half of 2025, especially in the Sun Belt region.5

Economists forecast that the median U.S. home price will remain flat in the third quarter and dip about 1% year-over-year by the end of 2025.8 Sellers are beginning to accept that sky-high comps from 2021 and 2022 are no longer relevant–-largely due to persistent affordability challenges.

Households earning $75,000 a year can now afford just 20% of homes on the market—down sharply from nearly 50% before the pandemic.¹ This shift is driven in part by a chronic shortage of housing supply, which continues to keep prices out of reach for many would-be buyers despite recent softening.10

This ongoing supply shortage is expected to prevent a significant drop in home values. As finance expert Michael Ryan tells Newsweek in May, “The housing market isn’t crashing dramatically, more like it’s finally coming back down to earth from a sugar high.”5

What it means for you: For buyers, softening prices can lead to better opportunities—especially in market segments where listings are lingering.

For sellers, the key is realism. “Gone are the days when you could slap any old price on your house and expect a bidding war,” says Ryan. Strategic pricing from the start is crucial. We can help determine what your home is truly worth in today’s market.5

LET’S MAKE YOUR NEXT MOVE A SMART ONE

While national housing reports can give you a “big picture” outlook, much of real estate is local. And as local market experts, we know what's likely to impact sales and drive home values in your particular neighborhood.

If you're planning to buy a home in 2025, you have more options and room to negotiate—but must remain vigilant about financing and affordability. If you're a seller, your strategy should reflect today’s conditions, not yesterday’s highs. And if you’re a homeowner, now is a good time to evaluate whether it makes sense to stay put, refinance, or take advantage of current equity to make a move.

The best decision is an informed one, and that’s where a trusted real estate professional comes in. We have the local insight, negotiation skills, and market knowledge to help you succeed—whether you're buying your first home, selling your third, or simply weighing your next move. Reach out today to start a conversation about your goals and how the current market can work for you.

The above references an opinion and is for informational purposes only. It is not intended to be financial, legal, or tax advice. Consult the appropriate professionals for advice regarding your individual needs.

Sources:

1. National Association of Realtors - https://www.nar.realtor/newsroom/americas-housing-affordability-gap-persists-households-earning-75000-annually-can-afford-less-than-a-quarter-of-for-sale-home-listings

2. Zillow -

https://www.zillow.com/research/home-value-sales-forecast-33822/

3. National Association of Realtors -

https://www.nar.realtor/research-and-statistics/housing-statistics/existing-home-sales

4. MarketWatch -

https://www.marketwatch.com/story/home-buyers-are-finding-the-silver-lining-in-a-stalled-housing-market-especially-if-theyre-in-this-group-1bd9eaff

5. Newsweek -

https://www.newsweek.com/map-shows-home-values-dropping-half-country-housing-market-shifts-2074904

6. National Association of REALTORS® Residential Economic Issues & Trends Forum -

https://www.nar.realtor/newsroom/nar-chief-economist-lawrence-yun-says-mortgage-rates-fast-rise-hurt-housing-market-during-realtors-legislative-meetings

7. National Association of REALTORS® Legislative Meetings 2025

https://cms.nar.realtor/sites/default/files/2025-06/2025-realtors-legislative-meetings-residential-economic-issues-and-trends-forum-lawrence-yun-presentation-slides-06-03-2025.pdf?_gl=1*166ceye*_gcl_au*MTUxMjAyMjU3Ny4xNzQ2ODI4MDcz

8. Redfin -

https://www.redfin.com/news/home-price-forecast-decline-2025/

9. ResiClub -