Can You Really Trust Online Home Estimates?

For millions of homeowners, checking their Zillow Zestimate has become as routine as checking a stock portfolio—a quick hit of seeing your home's estimated value, right at your fingertips. With 178 million monthly users and over 100 million homes covered, the platform's instant, free, and convenient appeal is undeniable.

But here's a famous cautionary tale: Spencer Rascoff, Zillow's former CEO, sold his own home for a staggering 40% less than its Zestimate. This story highlights a critical fact that many homeowners don't realize: Zillow itself calls its Zestimate a "starting point... not an appraisal"1.

If the creator of the system can be off by that much, how accurate are online home valuations for the rest of us? Relying on an automated number for your most valuable asset could be a mistake worth tens of thousands of dollars.

In this article, we'll examine how these powerful algorithms work, reveal the data behind their wildly varying accuracy rates, identify what they systematically miss, and show why local human expertise remains irreplaceable when precision—and your equity—matters most.

How These Algorithms Actually Calculate Your Home's Value

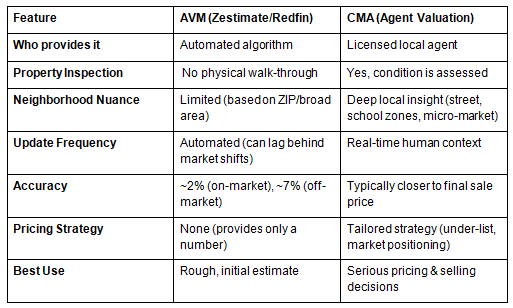

Automated Valuation Models are algorithms designed to crunch massive amounts of data in seconds.3 Think of them as sophisticated calculators—impressive in computational power, but limited by the quality and completeness of their inputs.

These systems analyze public records, tax assessments, recent comparable sales from the MLS, and basic property characteristics like bedrooms, bathrooms, and square footage.4 For standard properties with plenty of recent comparable sales, this data-driven approach can produce reasonable estimates.

But here's the fundamental limitation that shapes everything else we'll discuss: these models rely purely on historical data and never actually visit your property. They're backward-looking by design, using what sold yesterday to predict what might sell tomorrow, and while an algorithm can tell you that your home has three bedrooms, it cannot tell you that the primary suite has stunning morning light that makes buyers fall in love.

Accuracy and When Online Estimates Miss the Mark

Now for the numbers that every homeowner needs to understand.

When discussing AVM accuracy, you'll encounter the term "median error rate." This measures how far the estimate typically deviates from the actual sale price—specifically, half of all estimates fall within this percentage, and half fall outside it.2 Lower is obviously better, but context is everything.

The On-Market vs. Off-Market Divide

Here's where online home estimate accuracy gets interesting—and where most homeowners make their biggest mistake.

When a home is actively listed for sale, AVMs perform surprisingly well. Zillow's median error rate drops to just 1.83%–1.94%, while Redfin achieves 1.98%.2,5 These are impressive numbers. Why? Because when your home hits the market, these algorithms gain access to fresh, verified MLS data—professional photos, detailed descriptions, and real-time pricing intelligence.

For off-market properties—which describes your home right now if you're just curious about its value—the median error rate skyrockets. Zillow's accuracy drops to 7.06%–7.5%, while Redfin's plummets to 7.66%–7.72%.2,5 That's not a minor adjustment. That's a fundamental breakdown in reliability.

What This Means in Actual Dollars

Let's make this tangible. On a $400,000 home, a 7% median error translates to ±$28,000 or more—and remember, that's the median, meaning half of all estimates miss by even more than that. For a $600,000 property, you're looking at potential discrepancies exceeding $40,000. For luxury homes, the gap can easily reach six figures. The difference between an accurate valuation and an algorithm's best guess could equal is immense—so it’s important to understand their limitations.

The Algorithm's Blind Spots: What Online Estimates Cannot See

If AVMs have access to so much data, why do they miss by such significant margins? The answer lies in what they can't measure.

The Condition Conundrum

This is the AVM's Achilles heel. Every algorithm must assume your home is in "average condition." Your newly renovated kitchen with custom cabinetry? Average. Your finished basement adding 600 square feet? Average. Your brand-new HVAC system? Average. Flip it around—deferred maintenance, a crumbling driveway, outdated bathrooms—all get the same treatment. This isn't minor—condition often accounts for significant price variations between otherwise identical properties.

Location Nuances and Human Appeal

Algorithms understand neighborhoods but struggle with subtleties. Two identical homes—one on a quiet cul-de-sac, another backing a busy road. Same value to an algorithm, vastly different to buyers.

Market Lag and Unique Properties

Because AVMs depend on historical sales data, they lag behind current conditions. In rapidly moving markets, this lag can render estimates nearly useless. For custom homes, luxury properties, or anything unique, AVMs often fail completely—there simply aren't comparable sales to analyze.

The Solution: Why a CMA Is the Indispensable Tool

A Comparative Market Analysis (CMA) is the professional valuation tool that real estate agents provide. It's the bridge between raw data and real-world value—combining analytical power with human expertise and local knowledge.

What Makes a CMA Superior

Physical Inspection: Unlike an algorithm, your agent actually walks through your home. They see the quality of updates, evaluate floor plan flow, notice natural light, and assess the overall "feel" that influences buyer psychology. They identify value-adding features no database captures.

Micro-Local Knowledge: Agents live and breathe their local markets. They know which streets command premiums, understand seasonal patterns and inventory levels, and track current buyer demand. They explain not just what your home is worth, but why—and how to position it strategically.

Real, Adjusted Comparables: Your agent doesn't just pull recent sales—they analyze and adjust them. They can justify why your home is worth $20,000 more than one down the street: "Their kitchen had 1990s oak cabinets; yours has modern shaker style buyers want, justifying a $15,000 adjustment. They had builder-grade carpet; you have refinished hardwood, worth another $10,000."

Why Pricing Correctly From Day One Matters

For sellers, an accurate CMA prevents the two most expensive mistakes. Overpricing based on an inflated estimate leads to your home sitting stagnant—each week without offers damages your negotiating position and ultimately results in selling for less than if you'd priced correctly initially. Underpricing based on a conservative algorithm means leaving tens of thousands on the table. In real estate, you rarely get a second chance at a first impression. The initial listing price sets market perception, and getting it right requires the precision only a CMA provides.

When Online Valuations are Useful

For Sellers: Never set your listing price based solely on an online estimate. Use it as a conversation starter, but rely on your agent's CMA to build a strategic, defensible pricing plan.

For Buyers: Use online estimates to establish a general ballpark before you start searching, but trust your agent's analysis of recent comparable sales when crafting offers. The algorithm doesn't know that three other buyers are submitting offers this weekend—your agent does.

BOTTOMLINE: Technology Is a Tool, Not a Guide

Online home valuations are impressive tools for satisfying curiosity, but they remain prone to significant error—especially for off-market properties where median error rates of 7-8% translate to tens of thousands of real dollars. The blind spots around condition, location nuances, and market timing aren't minor technical limitations—they're fundamental gaps that only human expertise can fill.

When it comes to your largest financial asset and a decision that will impact your life for years, technology can give you a ballpark, but only a professional CMA can give you the strategic precision you need.

Ready to know what your home is really worth? Contact us today for a complimentary Comparative Market Analysis—a personalized, in-person valuation that examines your specific property, incorporates current market dynamics, and provides the strategic guidance the internet simply cannot match.

Sources

1. Inman - https://www.inman.com/2016/05/18/zillow-ceo-spencer-rascoff-sold-home-for-much-less-than-zestimate/

2. Zillow Zestimate Accuracy - https://www.zillow.com/z/zestimate/

3. Rocket Mortgage: Automated Valuation Model - https://www.rocketmortgage.com/learn/automated-valuation-model

4. Experian: What Is an Automated Valuation Model - https://www.experian.com/blogs/ask-experian/what-is-automated-valuation-model/

5. Redfin - https://www.redfin.com/redfin-estimate