5 ROADBLOCKS TO AFFORDABLE HOMEOWNERSHIP (AND WAYS TO MOVE PAST THEM)

Dreaming of a new home but feeling priced out? You’re not alone! According to a recent survey by Bankrate, 78% of aspiring homebuyers cite affordability issues as their primary deterrent.1

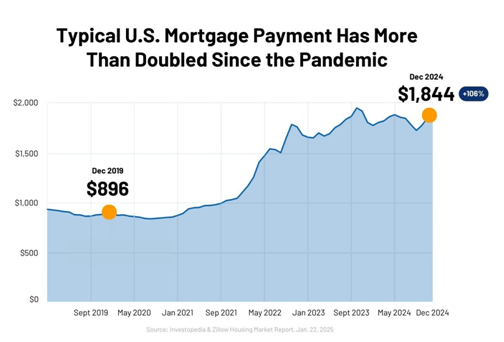

According to data from the U.S. Census Bureau, home prices have risen around 32% since the pandemic, and elevated mortgage rates have caused monthly payments to balloon.2

Despite the challenges, homeownership remains a top goal for many Americans. Fortunately, there are ways to turn your dreams of homeownership into reality! In this guide, we’ll explore five common roadblocks to affordable homeownership and actionable solutions to help you overcome them. Let’s break down those barriers so you can finally get the home of your dreams!

ROADBLOCK #1: I Don't Have Enough Saved For A Down Payment

Many prospective buyers believe they need a 20% down payment to buy a home. But in reality, most conventional loans require just 3-5%. And, for buyers who qualify, there are a number of programs and mortgage options that can make a home purchase more accessible.

Down Payment Assistance Programs (DPAs)

DPAs offer grants, loans, and other financial assistance to help with your down payment and closing costs. Many programs are specifically designed for first-time buyers, but there are also options for repeat homebuyers.3,4 These programs can significantly reduce the upfront costs of buying a home. We can help you find down payment assistance programs. Contact us to find out if you may qualify!

0% Down Government-Backed Mortgages

If you qualify for certain government-backed mortgages, you may not need to come up with a down payment at all.5 While these loans, offered by the Department of Veterans Affairs (VA) and the United States Department of Agriculture (USDA), are not available to all buyers, they offer numerous benefits, including competitive rates and no down payment requirement.

- VA loans are available to U.S. military members, including veterans and surviving spouses.6 They do not require a down payment, though the buyer must pay a fee at closing.

- USDA loans are available to moderate to low-income buyers in certain rural areas.7 They do not require a down payment.

Family Gifts

Did you know that 25% of first-time buyers in 2024 reported receiving down payment gifts or loans from family members or friends?8 In fact, a growing number of Baby Boomers are choosing to gift all or a portion of their heirs’ inheritance before they pass away.9 Some financial advisors even recommend this as part of their client’s estate plan. Just be sure to follow the proper procedures to document these types of gifts, if you’re fortunate enough to receive them.10

Existing Home Equity

Due to record-high real estate gains over the past few years, if you already own a home, you may have more equity than you realize.11 This equity (or difference between your home’s current value and what you owe on your mortgage) could go toward a down payment on a new property. Wondering how much equity you have in your current home? Reach out for a free home value assessment.

ROADBLOCK #2: I Can't Afford the Monthly Payment

Worried about those monthly mortgage payments? High interest rates and rising costs can make mortgage payments feel daunting. But there are strategies to reduce your monthly burden.

Explore Alternative Mortgage Terms

The traditional 30-year fixed-rate mortgage isn’t the only kind of loan out there. Options like adjustable-rate mortgages (ARMs) or hybrid mortgages can offer lower initial rates.12, 13 Some buyers opt for these if they plan to sell the home before the initial rate term ends or refinance down the road. A lower mortgage rate can significantly lower your monthly payment. However, it’s important to understand the risks involved so you can weigh the pros and cons before deciding.

Consider Discount Points

Buying discount points—a process also known as a permanent rate buy-down—is another great way to limit your monthly costs.14 Essentially, this strategy involves prepaying a fee to lower your interest rate across the life of your loan. If a seller is especially motivated, they may be willing to pay for discount points for the buyer to close the deal on a home. In some cases, we can help you negotiate these types of seller concessions.

Ask About Seller Financing or an Assumable Mortgage

Here are two less common options you might not have considered:15

- Seller Financing – The seller acts as the bank, offering you potentially better terms than a traditional mortgage.

- Assumable Mortgage – You take over the seller's existing mortgage with a lower interest rate than what's currently offered by lenders.

Note that these options may or may not be possible for you depending on the seller, the home, and the type of mortgage, but they are worth exploring—and we can help.

Co-Buy with Family or Friends

A growing number of homebuyers are returning to multigenerational living or are even buying a home with friends.16 This arrangement enables you to cut costs significantly while sharing both the time and financial responsibilities of homeownership. We can help you search for homes that are well suited for your group.

Purchase a Home with Income Potential

You can generate extra income to offset your mortgage payments by purchasing a duplex, renting out a room or an accessory dwelling unit (like a garage apartment), or even listing your property on Airbnb. We work with investors and can help you find a property to meet your goals.

ROADBLOCK #3: I Can't Qualify for a Mortgage

Qualifying for a mortgage can be a stressful process, especially if you have previously faced financial challenges. But you might be pleasantly surprised—there’s a lot you can do to improve your chances of success.

Boost Your Credit Score

Your credit score is foundational when it comes to getting a mortgage.17 A higher score typically means a lower interest rate and more options. Take steps to improve your credit by paying bills on time, reducing debt, and checking your credit report for errors. Even a small improvement in your score can make a big difference. Pro tip: Avoid opening or closing credit cards or taking out other loans (like car or personal loans) if you plan to start home shopping in the near future.

Lower Your Debt-to-Income Ratio

Lenders want to see that you can comfortably handle your debts. They assess this by calculating your debt-to-income ratio: your total monthly loan payments (including mortgage, car loans, student loans, and credit cards) divided by your gross monthly salary.18 Paying down other types of debt, like your car loan, will leave more space in your budget for a monthly mortgage payment.

Apply for an FHA Loan

FHA loans are designed for buyers with less access to savings, as well as those with lower credit scores.19 Down payments on FHA mortgages can be as low as 3.5% with a credit score of 580 or above, or 10% with a credit score of 500 or above. Generally, the buyer’s debt-to-income ratio must be below 43%, with no more than 31% of income going to mortgage payments. These loans do come with some additional requirements, such as mortgage insurance (including an upfront premium of 1.75% at closing), a pre-purchase inspection, and borrowing limits that vary based on geographic area.

Consider Getting a Co-Signer

Having a co-signer with a stronger credit history or more income can strengthen your application, but make sure you (and they) understand the risks and responsibilities involved.

ROADBLOCK #4: I Can't Find a Home in My Price Range

Feeling frustrated by the lack of affordable homes on the market? Unfortunately, this is a common problem.20 But with a little flexibility and guidance, it’s possible to find a great property to fit most budgets.

Expand Your Home Search

You may need to search outside your target area. In many markets, home prices vary drastically within the span of miles.21 Being open to exploring alternative neighborhoods or those farther from town can open up surprising possibilities. As local market experts, we can help you discover hidden gems and up-and-coming neighborhoods. Reach out for a complimentary consultation.

Revisit Your Must-Haves

Take a close look at your "must-have" list. Are there any features you can compromise on to expand your options and find a more affordable property? For example, do you really need two bathrooms, or could you settle for a single bathroom with space to add a second one in the future? These types of compromises can sometimes shave tens of thousands off your purchase price.

We’re happy to offer our thoughts on the features that you’re likely to find within your budget.

Consider Fixer-Uppers

Looking to cut purchase costs? Don't shy away from homes that need a little TLC.22 Fixer-uppers usually come with a lower price tag, and you can personalize the renovations to your taste. Just be sure to factor in the cost of repairs and renovations when determining your budget—and to be realistic about your own home repair skills! If you’re interested in exploring fixer-upper opportunities, we can help you identify properties with potential and connect you with reliable contractors.

ROADBLOCK #5: I'm Overwhelmed by the Process

Buying a home can feel like navigating a maze. Between searching for properties, securing financing, negotiating contracts, and handling paperwork, the process can quickly become overwhelming. But you don’t have to do it alone! We can simplify every step, helping you stay organized, informed, and confident in your decisions.

Find the Right Home Faster

The sheer number of listings on the market can be daunting, and homes that meet your criteria may not always be easy to find. Our team can:

- Save you time by narrowing down homes that fit your budget, needs, and lifestyle.

- Get you access to off-market and pre-listing properties that aren’t widely advertised.

- Provide insights on local market trends to help you make a competitive offer.

Navigate Financing & Paperwork With Ease

Real estate transactions involve complex contracts, legal documents, and lender requirements. One misstep could delay your purchase—or even cost you your dream home. We will:

- Help you find down payment assistance or grants that you may not be aware of.

- Explain mortgage options and connect you with reputable lenders.

- Ensure all purchase documents are accurate and deadlines are met.

Score the Best Deal

Many buyers worry about overpaying for a home or getting stuck with costly repairs, but we know how to:

- Use expert negotiation tactics to secure the best possible price.

- Identify hidden costs so you aren’t caught off guard at closing.

- Negotiate repairs or seller concessions to save you money.

Streamline Inspections & Closing

The home inspection and closing process can bring last-minute surprises. We avoid these by:

- Helping you interpret inspection reports and advising on necessary repairs.

- Coordinating with lenders, appraisers, and title companies to keep everything on track.

- Preparing you for closing day so you know exactly what to expect.

Benefit From Ongoing Support

Our relationship doesn’t end once you get the keys. We always go the extra mile to:

- Recommend trusted contractors for renovations and repairs.

- Help you make strategic upgrades through complimentary real estate consultations.

- Provide market updates in case you want to refinance or sell later.

The bottom line? You don’t have to navigate this process alone. When you work with us, you’ll have a trusted partner to handle the complexities, answer your questions, and ensure everything goes smoothly from start to finish.

LET’S TURN ROADBLOCKS INTO STEPPING STONES TOWARD YOUR DREAM HOME

Buying a home may come with challenges, but none of them are impossible to overcome. With the right strategies, resources, and expert guidance, you can navigate these obstacles with ease.

Whether you're worried about saving for a down payment, qualifying for a mortgage, or finding the right home in your price range, there are solutions available to help you move forward. The key is to stay informed, explore all your options, and work with professionals who can guide you every step of the way.

Our team is here to help you find the right home, secure the best financing, and negotiate the best deal—without the stress and uncertainty of doing it all yourself. Let’s turn your homeownership dreams into reality. Contact us today to get started!

The above references an opinion and is for informational purposes only. It is not intended to be financial, legal, or tax advice. Consult the appropriate professionals for advice regarding your individual needs.

SOURCES:

1. Bankrate -

https://www.bankrate.com/mortgages/home-affordability-report/#unaffordability

2. Nerdwallet -

https://www.nerdwallet.com/article/mortgages/2025-home-buyer-report

3. Bankrate -

https://www.bankrate.com/mortgages/first-time-homebuyer-grants/#types

4. Down Payment Resource -

https://downpaymentresource.com/

5. Bankrate -

https://www.bankrate.com/mortgages/types-of-mortgages/#government-backed

6. Bankrate -

https://www.bankrate.com/mortgages/understanding-va-loans/

7. Bankrate -

https://www.bankrate.com/mortgages/what-is-a-usda-loan/

8. National Association of Realtors -

https://www.nar.realtor/research-and-statistics/research-reports/highlights-from-the-profile-of-home-buyers-and-sellers

9. Business Insider -

https://www.businessinsider.com/boomers-not-waiting-pass-inheritance-wealth-transfer-millennials-need-it-2024-7

10. Experian -

https://www.experian.com/blogs/ask-experian/down-payment-gift-rules/

11. Bankrate -

https://www.bankrate.com/home-equity/homeowner-equity-data-and-statistics/

12. Nerdwallet -

https://www.nerdwallet.com/article/mortgages/adjustable-rate-mortgage-arm

13. Lending Tree -

https://www.lendingtree.com/home/mortgage/what-is-a-hybrid-mortgage/

14. Investopedia -

https://www.investopedia.com/terms/d/discountpoints.asp

15. Lending Tree -

https://www.lendingtree.com/home/mortgage/what-to-know-about-owner-financing/

16. National Association of Realtors -

https://www.nar.realtor/blogs/economists-outlook/home-for-the-holidays-the-rise-of-multi-generational-home-buying

17. Consumer Financial Protection Bureau -

https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/

18. Nerdwallet -

https://www.nerdwallet.com/article/mortgages/debt-income-ratio-mortgage

19. Bankrate -

https://www.bankrate.com/mortgages/what-is-an-fha-loan/#requirements

20. Bankrate -

https://www.bankrate.com/real-estate/low-inventory-housing-shortage/

21. Realtor -

https://www.realtor.com/advice/buy/priced-out-of-dream-neighborhood-cheaper-alternative/

22. This Old House -

https://www.thisoldhouse.com/buying/21017198/buying-a-fixer-upper-house